Cost-smoothing is a simple idea. Instead of a $400 healthcare bill landing all at once — on a Tuesday, when the paycheck isn’t until Friday and the HSA balance is at $240 or the HRA is tapped — the payment can be spread across future paychecks in small, interest-free installments to help ease the financial burden. No worries. No deferred care. Just a better match between when a bill arrives and when it actually gets paid. The concept isn’t complicated. And employees love it.

The Policy Moment and Affordability Tools discussed in our first broker blog are making big strides toward improving price transparency and eventual healthcare cost savings. But a price must be transparent and transactable- – in other words, fitting into an individual’s real budget so the prescription can be filled in full or an MRI can happen the same day it’s ordered. Whether those eventual savings materialize comes down to one question: Can the employee actually pay for the care they need at the moment it arrives?

Your clients have likely built great benefits stacks thanks to your help. Most include at least one of the tools we will walk through. Each has real value. Each has limitations. Pairing them with a payment solution that offers instant healthcare purchasing power and cost-smoothing with no interest or fees can reduce your clients’ healthcare costs and make their affordability tools work better for their employees. Before looking at those tools, it’s worth understanding who’s in your clients’ workforce for context — and what healthcare is already costing them.

The Income Reality Inside Every Employer Plan

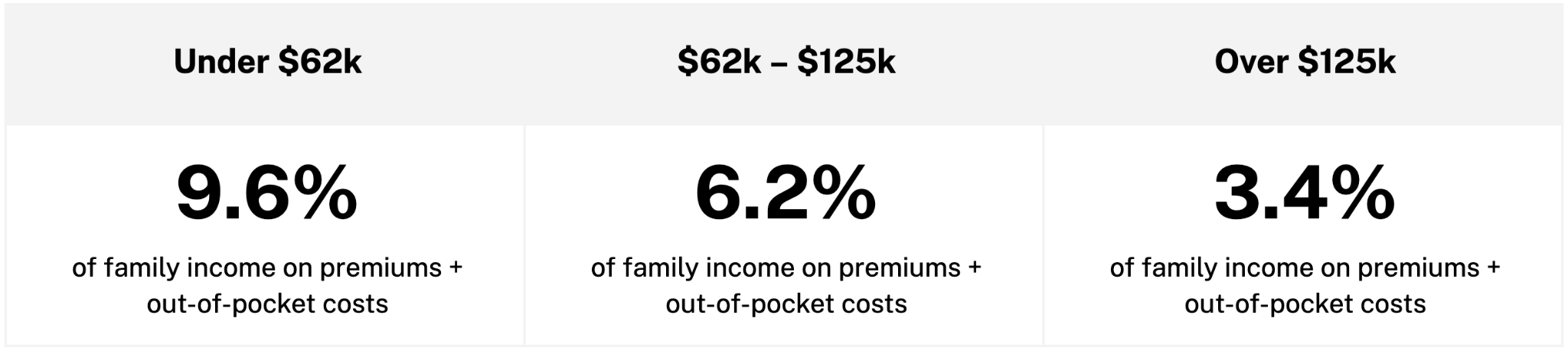

KFF’s June 2025 research on employer coverage affordability found three distinctly different financial experiences sitting inside the same health plan. Families earning under $62,000 spend an average of 9.6% of family income on premiums and out-of-pocket costs combined. The middle tier, $62,000 to $125,000, spends 6.2%. Above $125,000: 3.4%.

Source: Peterson-KFF Health System Tracker, June 2025 · healthsystemtracker.org

The benefits associated with the affordability tools below follow the same trajectory. They work progressively better as income rises. They are least effective for employees who need them the most. Let’s keep that in mind as we walk through each one.

The Health Savings Account (HSA)

Outstanding long-term tool when there is a sufficient balance to help pay for the needed care.

The HSA is excellent for employees who’ve had time to build a balance. Triple tax advantage, indefinite rollover, investment potential, portable across employers and plans. For someone contributing consistently for several years, it’s one of the best financial instruments in the entire benefits stack.

The picture on the ground is simply uneven. Only 33% of covered workers had an HSA in 2025. The tool and its inherent savings benefits are most available to the employees with disposable income and those who can afford to put money aside to save.

The income dimension the aggregate data doesn’t capture is evident when looking a bit deeper. Service workers — typically the lowest-paid occupational group — have only 22% HSA access. Management and financial workers have 61%. In addition, the Employee Benefit Research Institute finds that roughly 55% of HSA-eligible enrollees contribute $0 of their own money to the account in a given year, choosing instead to keep that money in their paycheck to cover non-medical living expenses. The extra take-home pay is often the draw and they’re more willing to take a chance they can remain healthy for it.

Pairing an HSA with cost-smoothing capabilities completes the solution

When the HSA balance can’t cover the medical bill, or employees prefer to build their HSA savings for retirement coverage, a healthcare payment solution like Paytient enables employees to pay the cost of their bills over time – always without interest or fees. Healthcare happens when it’s needed. The HSA keeps accumulating — untouched, building toward the balance it was designed to hold.

The Flexible Spending Account (FSA)

Efficient for what you can predict. Less so for what you can’t.

The FSA gives employees the full year’s election on day one, funded pre-tax. For predictable expenses — a planned procedure, regular prescriptions, scheduled dental work — it delivers real efficiency and genuine tax savings. That’s worth recognizing.

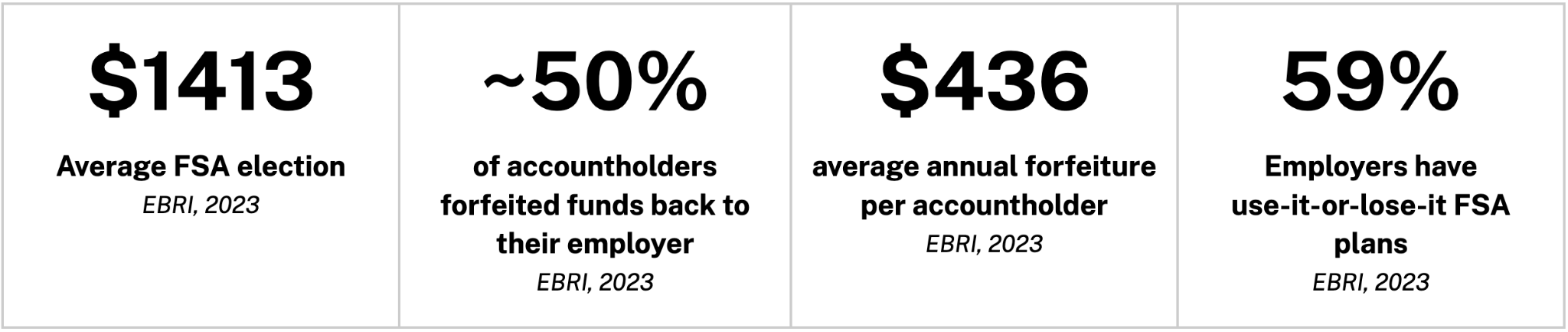

The structural challenge is what the FSA asks employees to do: forecast their healthcare year before the plan year and commit to a dollar amount they can’t change. The use-it-or-lose-it rule can make for stressful, and often unfortunate, decisions as people struggle to forecast their healthcare needs. The data clearly supports that finding with around 50% of FSA account holders forfeiting unused dollars, averaging $436 each per year.

One structural note worth flagging for plan design conversations: employees in a general-purpose FSA can’t contribute to an HSA in the same year — the IRS treats the two as mutually exclusive. Many employees don’t know they’re making that choice at enrollment. A limited-purpose FSA covering dental and vision only can coexist with an HSA, but that requires deliberate plan design.

Pairing an FSA with additional healthcare purchasing power can also mitigate employee risk of under-investing

When the unplanned expense arrives after the balance has been drawn down, a healthcare payment solution like Paytient provides additional purchasing power to be used with cost smoothing flexibility to help those employees pay for the remainder of their medical costs over time. No deadline. The employee gets care regardless of their forecast accuracy.

The Health Reimbursement Arrangement (HRA)

Real employer commitment – with a ceiling.

The HRA is entirely employer-funded — no employee contribution required, no enrollment decision to make. Whatever the employer puts in, the employee benefits from. That's genuine investment in workforce health, and it's worth acknowledging plainly.

The KFF 2025 Employer Health Benefits Survey shows the HRA doing meaningful work for the majority of workers it serves. 33% of covered workers in HRA-paired HDHPs receive an employer contribution equal to or greater than their full deductible. A further 19% receive contributions that, if applied to their deductible, bring their remaining annual liability below $1,000.

That leaves 48% with >$1,000 out-of-pocket exposure the HRA doesn't resolve — and that's the honest limitation. For these employees, the employer contribution runs out before the deductible does. The HRA has a ceiling, and once it's reached, the remainder falls to the employee. Deeper into the plan year, when the HRA has been drawn down and the next enrollment is months away, there's no more employer contribution coming until the plan resets.

Pairing an HRA with the additional healthcare purchasing power extends the employees' ability to pay for their care

When the HRA ceiling is reached, employees can use Paytient’s healthcare purchasing power and cost-smoothing solution to pay for their remaining healthcare needs over time. The employer’s investment remains. The employee has a manageable path forward rather than a bill that exceeds their available balance in savings, providing for more manageable cash flow.

The Final Picture: Cost-Smoothing Saves Your Clients Money

Each of the three affordability tools excels at what it was designed for. The HSA builds long-term financial resilience. The FSA captures tax efficiency on predictable costs. The HRA expresses employer investment. None, however, were designed for the most critical employee pain point – an easier way to pay for the immediate out-of-pocket cost at the moment of care – when lump sum payments are difficult or just not possible – when prior contributions were not made or are no longer available.

Paytient’s healthcare payment solution is proven to help people get the care they need with 78% of members receiving care they otherwise would have delayed or skipped altogether – saving your clients money on high cost claims that appear later – with average potential savings of $600 per employee per year.

- Members shift from deferred care to on-time care

- Members shift from medication non-adherence to adherence

And with the advantages of available healthcare purchasing power with cost-smoothing, employers are seeing even more savings opportunities with more, healthier employees shifting to lower premium, higher deductible plans.

The Question Worth Asking Your Clients at Their Next Renewal

Your clients have the affordability tools. Each has real value. Each has limitations.

What is the plan to help employees pay for their healthcare when their limitations are reached?

Paytient’s healthcare payment solution is a perfect pairing to help your clients’ people continue to pay for their healthcare – at the most important moment – when care is needed.

To learn more about how Paytient can help your clients:

.webp)